TO: Interested Parties

FROM: Unlocking America’s Future and Build America Policy Council

DATE: July 23, 2025

RE: State Legislative Victories Show Responsible Investing Is Good Policy and Good Politics

State legislative sessions in 2025 have so far delivered a resounding message: responsible investing legislation represents both sound policy and winning politics, while anti-responsible investing attacks continue to fail because they fundamentally harm American families, workers, and businesses.

From deep-red Louisiana to politically dynamic states like North Carolina to blue Oregon, it’s clear that when lawmakers are forced to choose between protecting Americans’ financial security and advancing extremist agendas backed by billionaires and special interests, responsible investing policies prevail.

Here’s what you need to know about how responsible investing legislation has helped unlock America’s future:

The Political Landscape: Anti-ESG Legislation Fails Even in Favorable Environments

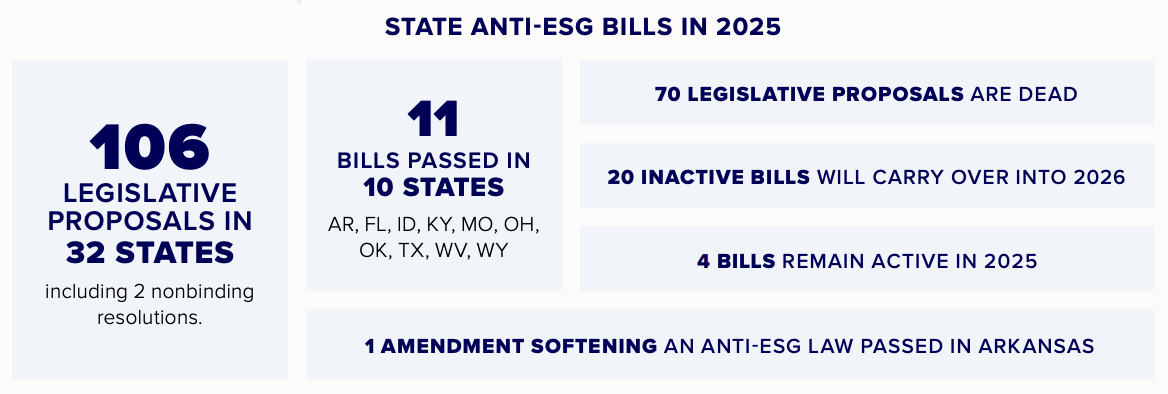

In the first six months of the 2025 legislative cycle, we’ve seen a decisive rejection of anti-responsible investing legislation nationwide. According to tracking by Pleiades Strategy, of the 106 anti-responsible investing bills introduced across 32 states, a staggering 70 legislative proposals died outright, with only 11 bills passing in 10 states. This represents a failure rate of over 65 percent, demonstrating the fundamental weakness of anti-responsible investing arguments when subjected to real-world scrutiny.

The most striking confirmation of the unpopularity of anti-responsible investing legislation comes from Louisiana, where anti-responsible investing legislation died despite operating in what should have been the most politically-favorable environment possible. Senate Bill 7 and House Bill 418, which would have stripped investment choices away from Louisiana’s teachers, firefighters, and police officers, failed to pass even in a deep-red state with a Republican supermajority. Extremists’ failure in deep-red Louisiana, even with the most politically advantageous circumstances, speaks volumes about the obvious economic destructiveness of anti-ESG legislation.

The pattern of failure extends far beyond Louisiana. In Iowa, proposed limitations on pension funds’ shareholder voting abilities created internal Republican conflict, with the state treasurer’s office raising concerns about provisions authored by the attorney general’s office. Similarly, Wyoming witnessed dramatic infighting between Republican officials, with Treasurer Curt Meier warning that proposed legislation would cause his entire investment staff to resign and leave the state “with nobody to invest and no markets to invest in.”

(Source: Pleiades Strategy 2025 Statehouse Report)

Even where anti-ESG bills advanced, they were often significantly watered down during the legislative process. In Missouri, HB 147 was amended to be largely rhetorical, prohibiting investing criteria only when they would “override fiduciary duties”—language that state retirement system officers confirmed would not change their current standards. Oklahoma’s SB 500 and West Virginia’s HB 3342 both received “escape clauses” allowing financial institutions to refuse services for “traditional business reasons,” effectively neutering their impact.

The consistent thread connecting these failures is that anti-responsible investing bills create real, tangible harm to working families while delivering benefits primarily to corporate interests and wealthy donors who fund these legislative efforts. When lawmakers must explain to constituents why their retirement savings should be put at risk to advance an ideological agenda, support for those bills drastically declines.

Texas: Massive Legislative Assault Largely Defeated

Texas provided perhaps the most dramatic example of how sustained advocacy and public pressure can defeat even the most coordinated anti-responsible investing campaigns. Despite facing nearly 30 separate anti-ESG bills introduced across both legislative chambers—representing an unprecedented assault on responsible investing practices—only three ultimately became law. This represents a massive victory for Texas families and demonstrates the power of organized resistance to these harmful proposals.

The scope of the legislative attack in Texas was shocking—bills targeted everything from university endowment investments to insurance regulations to shareholder rights, representing a comprehensive attempt to dismantle responsible investing infrastructure across multiple sectors of the Texas economy. The fact that more than two thirds of bills failed to become law, despite strong Republican control of the legislature, illustrates both the inherent weakness of anti-ESG arguments and the effectiveness of sustained advocacy efforts.

The bills that did pass in Texas reveal the true nature of anti-responsible investing legislation: corporate welfare disguised as populist policy. Senate Bill 1057, which raises ownership requirements for shareholder proposals to at least one million dollars in voting securities, effectively ensures that only billionaires and large institutional investors can hold corporations accountable. This represents a fundamental betrayal of the populist rhetoric that typically accompanies anti-ESG campaigns, exposing these efforts as pay-to-play schemes designed to protect wealthy corporate interests from accountability.

Similarly, Senate Bill 2337 undermines informed investment decision-making by preventing proxy advisors from considering material risks that could impact investment returns. By forcing advisors to ignore environmental, social, and governance risks—even when those risks have clear financial implications—this legislation actively harms Texas pension funds and individual investors. The contradiction between anti-ESG rhetoric about protecting investors and the actual impact of anti-ESG legislation could not be more stark.

Texas also demonstrates the importance of sustained engagement throughout the legislative process. Several bills that initially contained harmful anti-responsible investing provisions were ultimately stripped of those elements through advocacy efforts. House Bill 2067, for example, originally included language that would have prevented insurance companies from using proven risk assessment criteria, but the final legislation removed these provisions entirely. This represents a significant win for Texas families and shows how persistent advocacy can achieve meaningful policy improvements even in challenging political environments.

Oregon: Proactive Leadership on Responsible Investing

While defensive victories in Louisiana and Texas demonstrate the weakness of anti-ESG arguments, Oregon’s proactive approach to responsible investing legislation shows what positive policy leadership looks like in practice. Governor Tina Kotek’s signing of both House Bill 2081 and House Bill 3546—the POWER Act—into law represents a comprehensive approach to protecting both retirement security and energy affordability for Oregon families.

House Bill 2081 makes Oregon a national leader in protecting the retirement security of public employees by ensuring that pension investments for teachers, firefighters, police officers, and other public servants account for climate-related financial risks. This legislation, championed by Oregon State Treasurer Elizabeth Steiner and supported by a bipartisan coalition of lawmakers, demonstrates how responsible investing principles can be translated into concrete policy protections for working families.

The bipartisan support for HB 2081 is particularly significant because it shows how responsible investing transcends traditional partisan divides when framed correctly. By focusing on the practical benefits of considering all material risks in investment decisions—rather than getting bogged down in ideological debates—Oregon lawmakers were able to build broad coalition support for legislation that directly protects their constituents’ financial futures.

Similarly, the POWER Act will allow Oregon’s Public Utility Commission to establish separate rate classes for high energy use facilities, primarily data centers. This ensures that high-energy commercial users pay their fair share rather than passing costs onto everyday ratepayers—meaning responsible policy can simultaneously protect consumers and maintain competitive markets.

The Oregon victories also illustrate the importance of having strong champions in key positions. Treasurer Steiner’s leadership on pension investment protections shows how elected officials can use their platforms to advance responsible investing principles in ways that directly benefit their constituents. This kind of proactive leadership creates positive examples that other states can follow while building momentum for responsible investing policies nationwide.

North Carolina: Sustained Pressure and Public Education Keeps Bill from Moving Forward

Our ongoing campaign in North Carolina, including a six-figure advertising campaign targeting lawmakers, demonstrates how sustained public pressure can create real political costs for lawmakers considering anti-responsible investing legislation. The campaign, which included both digital and print components, highlighted the dangers of pending legislation that would force financial institutions to ignore material risks and create regulatory confusion across the state.

Focusing on the economic consequences of anti-ESG legislation helped emphasize the impacts, particularly how these bills would ”prioritize billionaires’ extreme agendas ahead of letting financial professionals do their jobs.” The campaign also highlighted North Carolina’s economic competitiveness concerns, noting how anti-responsible investing legislation would disadvantage the state’s ability to compete for future-focused industries and jobs.

This economic development angle is particularly powerful in states like North Carolina that are actively working to attract high-tech industries and skilled workers. When anti-ESG legislation is framed as potentially harmful to economic development efforts, it creates additional political pressure on lawmakers to reconsider their positions.

The sustained nature of the North Carolina campaign—building on previous efforts from 2024—shows the importance of long-term engagement on these issues. Anti-responsible investing legislation rarely disappears after a single defeat; instead, it tends to resurface in modified forms as proponents search for politically viable approaches. Maintaining consistent pressure and public education efforts as the North Carolina legislature reconvenes later this year will create an environment where lawmakers understand that backing anti-ESG legislation carries ongoing political costs.

Conclusion: Why Responsible Investing Wins

This pattern of pro-responsible investing legislation succeeding while anti-ESG bills fail across these states reveals several key insights about the political dynamics surrounding responsible investing legislation. Most importantly, responsible investing policies win because they align with voters’ fundamental values about fairness, economic security, and common-sense risk management. When presented with clear information about the benefits of considering all material factors in investment decisions, voters consistently support responsible investing approaches because it protects their bottom line.

Polling data consistently shows strong public support for responsible investing principles across partisan lines. These numbers reveal a fundamental disconnect between the priorities of anti-ESG activists and the concerns of ordinary Americans. While special interest groups and ideological organizations focus enormous resources on attacking responsible investing practices, voters are far more concerned with practical issues like retirement security, job creation, and economic competitiveness.

The economic arguments for responsible investing are particularly compelling because they address voters’ real-world concerns about financial security and economic opportunity. When responsible investing is framed in terms of lower costs for families, increased competitiveness for businesses, job creation in growing industries, and better risk management for retirement savings, it becomes difficult for opponents to mount effective counterarguments. Anti-responsible investing legislation, by contrast, typically requires voters to accept short-term economic costs that ignore real-word risks in service of ideological goals that may seem abstract or disconnected from their daily lives.

Corporate accountability also resonates strongly with voters who are increasingly skeptical of corporate power and influence. When anti-ESG legislation is revealed to primarily benefit wealthy corporate interests—as demonstrated by bills like Texas’s SB 1057 that effectively limit shareholder rights to billionaires—it becomes politically toxic even among voters who might otherwise be sympathetic to anti-ESG rhetoric.

The Bottom Line: The fundamental strength of the responsible investing movement—that it aligns with voters’ core values about economic security, fairness, and common-sense risk management—provides a solid foundation for continued success. As more states recognize the benefits of responsible investing policies and the costs of anti-responsible investing restrictions, the political momentum will continue building in favor of approaches that protect Americans’ investments while supporting long-term economic growth and competitiveness.